China’s GDP Climbs 5.4%, While Housing Slump Stabilizes

Week Ending January 17, 2025

China’s economy expanded by 5.4% year-over-year in Q4 2024, accelerating from 4.6% in Q3 and surpassing market expectations of 5.0%. This growth, driven by robust industrial production (+6.2%) and a rebound in retail sales (+3.7%), signals the impact of Beijing’s targeted stimulus measures despite persistent property market weakness. While the broader economy shows signs of resilience, property investment declined by 10.6% year-over-year, underlining structural challenges that continue to weigh on growth prospects.

⏱️ Global Markets in 10 Seconds:

🇺🇸 Core Inflation 3.2% slows as stocks rally strong 📈

🇪🇺 STOXX 600 +2.37% amid ECB rate cut expectations 🎯

🇬🇧 Inflation 2.5% cools while GDP growth lags at 0.1% ⚠️

🇨🇳 GDP +5.4% YoY as industrial output surges 6.2% 🚀

🇯🇵 Nikkei -1.9% pressured by yen strength and BoJ signals 💼

🔍 The Big Picture

This week highlighted a mixed global narrative, with optimism building in the U.S. and China while Europe faced ongoing structural challenges. Emerging markets showed resilience, but diverging stories across regions hint at complex economic dynamics ahead.

United States: Core inflation eased to 3.2%, marking progress toward the Fed’s 2% target. Stocks rallied, with value outperforming growth for the first time since September, but the Fed is unlikely to cut rates soon. Keep an eye on retail sales momentum, which showed a modest +0.4% gain but lagged expectations.

International: UK inflation slowed to 2.5%, sparking hopes for a February rate cut, while GDP rose only 0.1% in November, underwhelming forecasts. Meanwhile, German GDP contracted by 0.2% in 2024, signaling lingering headwinds for Europe’s largest economy.

Emerging Markets: China’s GDP growth hit 5.4% YoY in Q4, boosted by industrial output at +6.2%, yet property investment slumped -10.6%, underscoring structural weaknesses. Elsewhere, India maintained solid growth momentum, supported by strong domestic demand.

⭐️ Post of the week

This week, BlackRock Investment Institute shared a striking analysis of 10-year U.S. Treasury yields, highlighting an unusual dynamic: yields have been climbing since the Federal Reserve began cutting interest rates in September 2024. This chart challenges the conventional wisdom that rate cuts invariably lower yields, underscoring how today’s macroeconomic environment diverges from historical patterns.

Source: Axel Christensen - Linkedin

Why This Analysis Matters

Framework Challenge: The chart juxtaposes the current trajectory of Treasury yields with past rate-cutting episodes, revealing that this cycle defies historical norms.

Market Assumptions Tested: It confronts the assumption that rate cuts are uniformly bullish for bonds, emphasizing how structural changes can rewrite market playbooks.

Interconnected Complexity: Rising term premiums and evolving global dynamics (e.g., fiscal pressures and geopolitical fragmentation) deepen our understanding of bond market behaviors.

Supporting Evidence:

Last Week’s Data: The 10-year yield touched 4.80%, its highest level in over a year, driven by robust U.S. labor market data and sticky inflation.

Historical Comparison: In past cycles, yields typically declined during rate cuts as lower rates reduced borrowing costs. Today, persistent fiscal deficits and rising term premiums are countering this trend.

Deeper Structural Factors: Elevated bond yields reflect market demands for higher compensation amid long-term risks like corporate refinancing at higher rates and fiscal policy uncertainty.

Bottom Line

This analysis is a masterclass in how structural factors can disrupt traditional market relationships. For investors, the key takeaway is clear: Always question assumptions and assess data within the broader macroeconomic context. Understanding these shifts is crucial for adapting investment strategies in today’s evolving regime.

💼 Market Indicators

SPY Performance

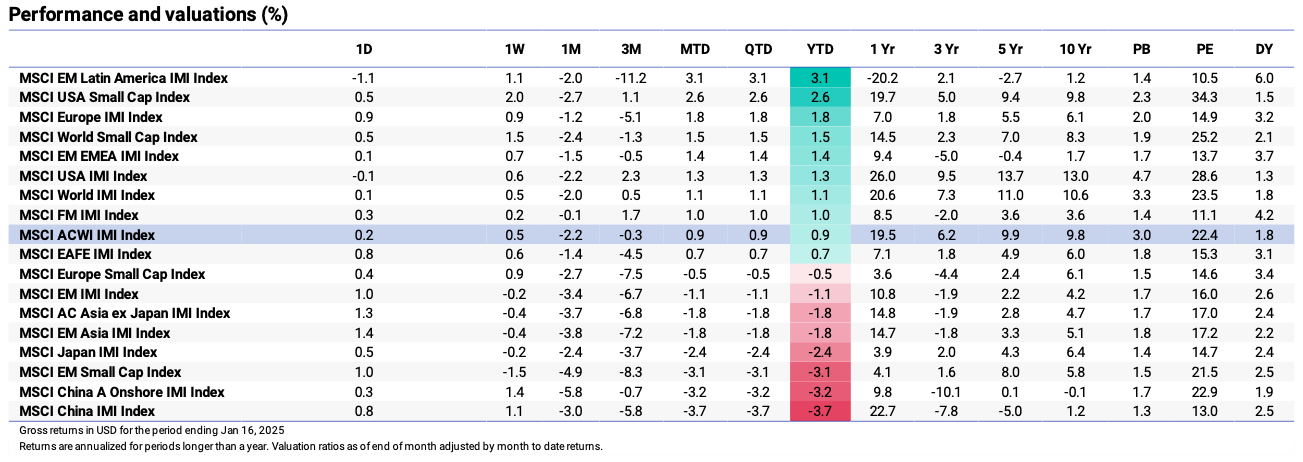

Performance and Valuations by Region

Source: MSCI

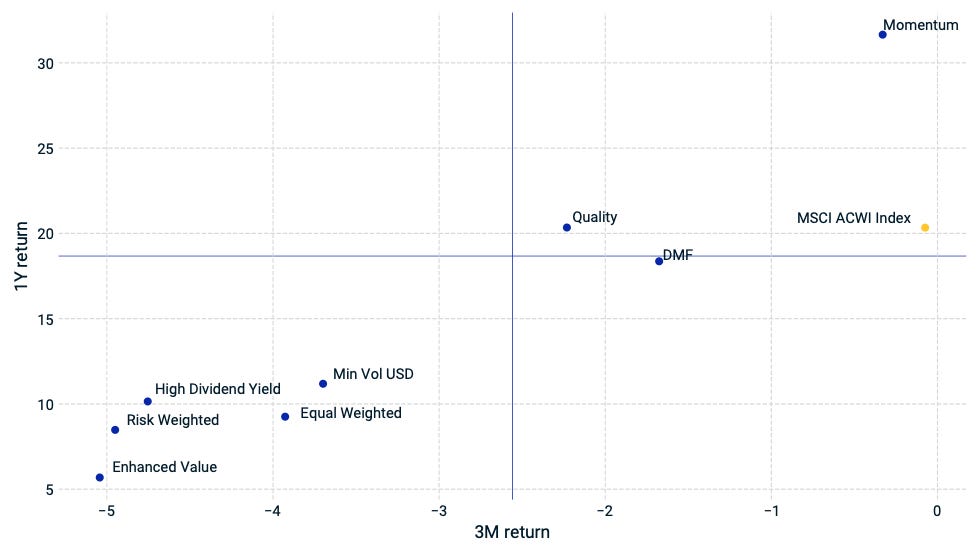

Momentum performance by Style

Source: MSCI

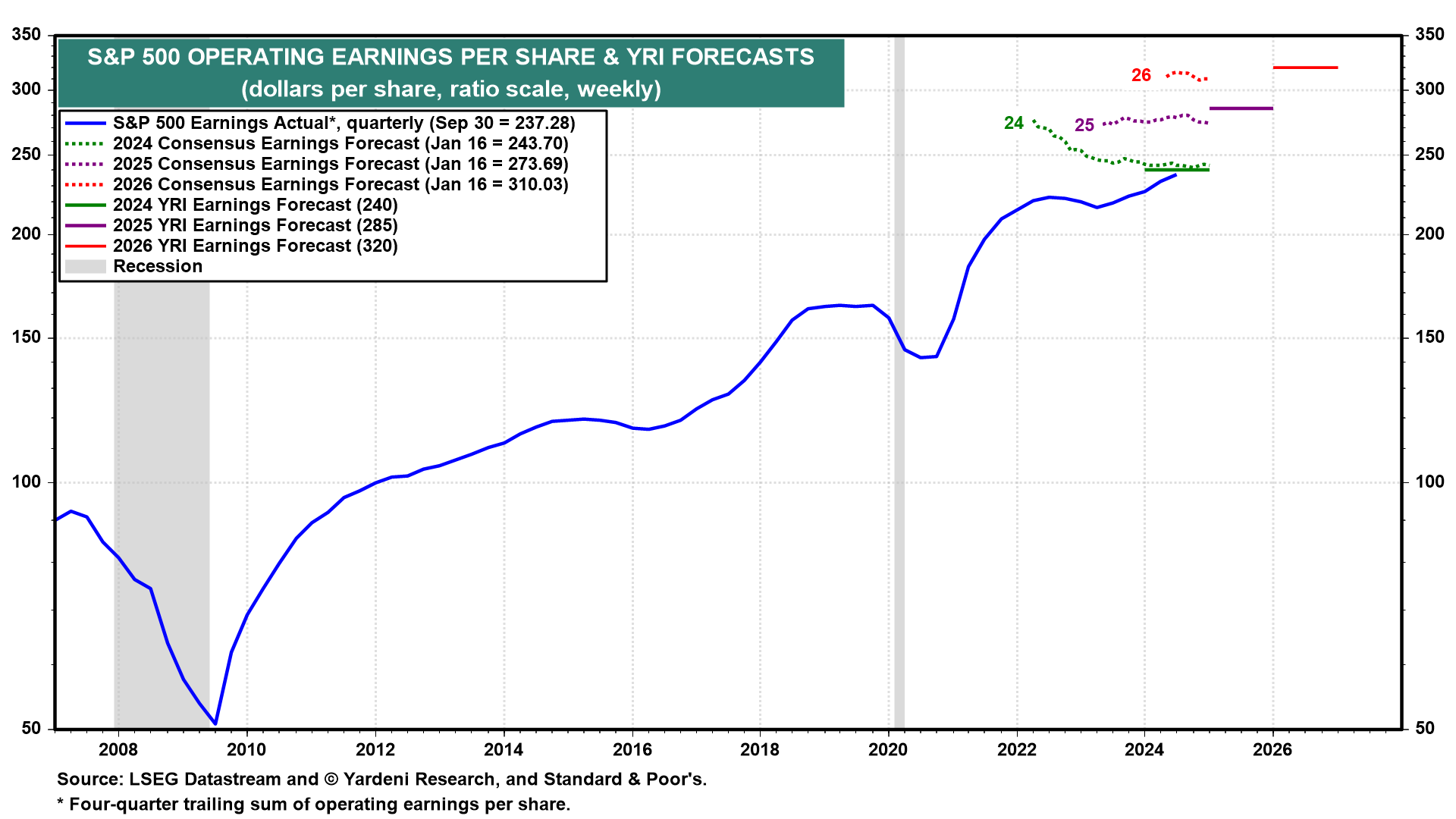

S&P 500 Earnings Per Share

Source: Yardeni Research

🗺️ Around the World in Detail

🇺🇸 United States: Manufacturing Under Pressure

Core Inflation at 3.2%: December's core inflation slowed to its lowest annual pace since July, signaling progress in the Fed's fight against rising prices. While this offers hope, it may not be enough to prompt immediate rate cuts, keeping monetary policy tight.

Retail Sales up 0.4%: December sales missed expectations of 0.6%, indicating cautious holiday spending. Strong gains in sporting goods and clothing helped offset weaker categories like building materials.

Bank Earnings Boost Stocks: Major banks like JPMorgan and Citigroup saw strong Q4 profit growth, driving financial stocks higher. This renewed optimism suggests resilience despite economic uncertainty.

🌐 International Markets: Diverging Paths

Canada 🇨🇦

Muted Week: No significant data releases or policy changes this week, leaving markets largely steady. Investors await upcoming housing data for clues on the economy’s trajectory.

Europe 🇪🇺

German GDP Down 0.2% in 2024: The second consecutive annual contraction underscores lingering economic weakness, particularly in investment spending. The ECB’s cautious rate cuts may not be enough to reignite growth.

Consumer Confidence Ticks Up: The STOXX Europe 600 Index climbed 2.37%, driven by optimism over falling inflation across the region. This may provide short-term relief but fails to resolve deeper economic fragilities.

United Kingdom 🇬🇧

UK Inflation Cools to 2.5%: December’s unexpected slowdown in inflation raises expectations for a February BOE rate cut, but stagnant GDP at just +0.1% in November suggests deeper structural challenges remain.

Japan 🇯🇵

Nikkei Falls 1.9%: Rising 10-year bond yields and yen strength, fueled by hawkish BOJ signals, weighed on equities. Export-heavy sectors face pressure as the yen gains to JPY 155.6 per dollar, complicating Japan’s growth story.

🌏 Emerging Markets: Recovery and Risks

China 🇨🇳

GDP at 5.4% YoY in Q4: Industrial output surged +6.2%, driving growth above expectations, while retail sales rebounded +3.7%. However, deep declines in property investment (-10.6%) highlight persistent structural issues.

Trade Surplus at $104.8B: Exports soared 10.7%, boosted by front-loaded orders ahead of tariff risks. This reflects near-term resilience but underscores dependency on external demand.

India 🇮🇳

Resilient Growth: India’s PMI stayed robust above 56, reflecting strong domestic demand. This positions India as a regional outperformer amid global uncertainties.

South Korea 🇰🇷

Unemployment Rises to 3.7%: Economic uncertainty and political turmoil pushed joblessness to its highest level since 2021, highlighting the challenges facing the country’s recovery.

Taiwan 🇹🇼

Stable Growth: With limited major data this week, Taiwan remains focused on trade resilience amid evolving geopolitical tensions in Asia.

🔑 Key Takeaway

This week’s data highlights the diverging dynamics shaping global markets, with inflation progress, fiscal strains, and structural shifts driving key narratives.

In the U.S., core inflation eased to 3.2%, boosting optimism for long-term price stability, yet sticky wage growth and cautious retail spending kept rate-cut expectations in check. Meanwhile, Europe faces contrasting signals: a slowing German GDP (-0.2%) and cooling UK inflation (2.5%) suggest room for policy easing, but structural growth challenges remain unresolved. China’s stronger-than-expected GDP growth (+5.4%), driven by industrial gains, contrasts with persistent weaknesses in property investment (-10.6%), underlining its reliance on policy stimulus and external demand.

As the Post of the Week emphasized, climbing U.S. Treasury yields despite rate cuts reflect broader structural pressures, reminding investors that traditional playbooks often fail in this evolving regime. Regional disparities and rising risks demand a sharp focus on interconnected forces and adaptability in portfolio strategies.

The content provided on MacroQuant Insights is for informational and educational purposes only and does not constitute financial advice. While every effort is made to ensure accuracy and reliability, all data, analysis, and opinions are based on sources believed to be trustworthy but are not guaranteed for completeness or timeliness. The views expressed are solely those of the author and do not reflect endorsements or recommendations for any specific investment, strategy, or action.

Investing involves inherent risks, including the potential loss of principal. Past performance is not indicative of future results. We strongly encourage readers to conduct their own research and consult with a qualified financial advisor or professional before making any financial decisions. MacroQuant Insights and its contributors disclaim all liability for investment decisions based on the information provided and make no warranties regarding the content’s accuracy or reliability.

Remember, all investments carry risks, and it is essential to understand these risks fully before acting on any information presented. Users are responsible for their own investment decisions. MacroQuant Insights assumes no responsibility for any outcomes resulting from the use of this information. Content is subject to change without notice.